.jpg)

Be Your Own Bank in 2026: How Smart Families Use the Debt Freedom Flywheel to Pay Off $50K While Building Wealth

- Reuben Lowing

- 9 hours ago

- 5 min read

The Prison You Didn't Know You Were In

Let's cut through the noise: You're funding someone else's empire while your own family starves.

Every month, you send checks to credit card companies, car lenders, and mortgage servicers. They call it "being responsible." I call it what it is, the Prison of Interest. You're not building wealth. You're building their quarterly earnings reports.

Here's the gut punch most financial "experts" won't tell you: Traditional debt payoff strategies (snowball, avalanche, consolidation) are designed to keep you in the game longer. They're treadmills disguised as escape routes. You pay off one debt while interest compounds on another. You celebrate small wins while the banking system celebrates your lifetime of payments.

The Myth: "Pay off your debt first, THEN start building wealth."

The Truth: That timeline keeps you broke for decades. By the time you're "debt-free," inflation has stolen your purchasing power and you've missed 10-15 years of compound growth.

The Warrior-Steward Mandate: Break the Cycle

In BUD/S, we learned a brutal lesson: Unrelenting pressure breaks every defense. The instructors didn't ease up. They didn't negotiate. They applied strategic force until you either evolved or quit.

Your debt requires the same approach, but with one critical difference: You're applying pressure on TWO fronts simultaneously.

This is the Debt Freedom Flywheel, and it's built on an ancient principle most modern advisors have forgotten: Stewardship isn't about hoarding or sacrificing, it's about strategic deployment.

Luke 16:11 asks the question that haunts every family drowning in payments: "If you have not been trustworthy in handling worldly wealth, who will trust you with true riches?"

Consumer debt isn't just a financial problem. It's a violation of the Law of Stewardship. It's evidence that your money is managing you instead of the other way around.

The Debt Freedom Flywheel: How to Pay Off $50K While Building Exponential Wealth

Here's what the banking system doesn't want you to understand: The same dollar can do double duty.

The Flywheel operates on two core principles:

1. The Knowing (Certainty of the Finished Work)

This isn't positive thinking. This is tactical certainty backed by mathematical inevitability.

When you structure an Equity Indexed Universal Life (EIUL) policy correctly, you create a private banking system with:

0% floor protection (your money doesn't evaporate in market crashes)

Participation in S&P 500 gains (capturing growth without downside risk)

Tax-free access to your cash value through policy loans

Compounding that never stops, even while you're borrowing against it

Your money doubles every 2.5 years at 28.9% average growth (Rule of 72: 72 ÷ 28.9 = 2.49). That's not a promise, it's wealth capacity mathematics.

Compare that to your credit card's 18-29% interest working AGAINST you. Same force. Opposite direction.

2. Unrelenting Pressure (Strategic Force Application)

You don't wait to start. You start while you're still in debt.

The Tactical Sequence:

Month 1-6: Fund your EIUL policy aggressively. Yes, while you're making minimum payments on everything else. This feels backwards. It's supposed to. You're building the weapon that will eliminate your debt faster than any snowball method ever could.

Month 7+: Take a policy loan against your accumulated cash value. Use it to obliterate your highest-interest debt (credit cards, personal loans). Your cash value continues earning 28.9% average annual growth. Your loan rate? Typically 5-8%.

The Arbitrage: You're earning 20%+ spread between what your money grows at and what you're paying to borrow it. That spread is exponential wealth generation.

The Repayment: As each debt falls, you redirect those former payments into two channels:

Repaying your policy loan (recapturing interest back into YOUR system)

Funding additional EIUL contributions (accelerating wealth capacity)

This is why we call it a Flywheel. Each rotation generates more momentum. Each debt you eliminate frees up cash flow that amplifies the next strike.

The Prison of Interest vs. The Sovereignty of the Private Bank

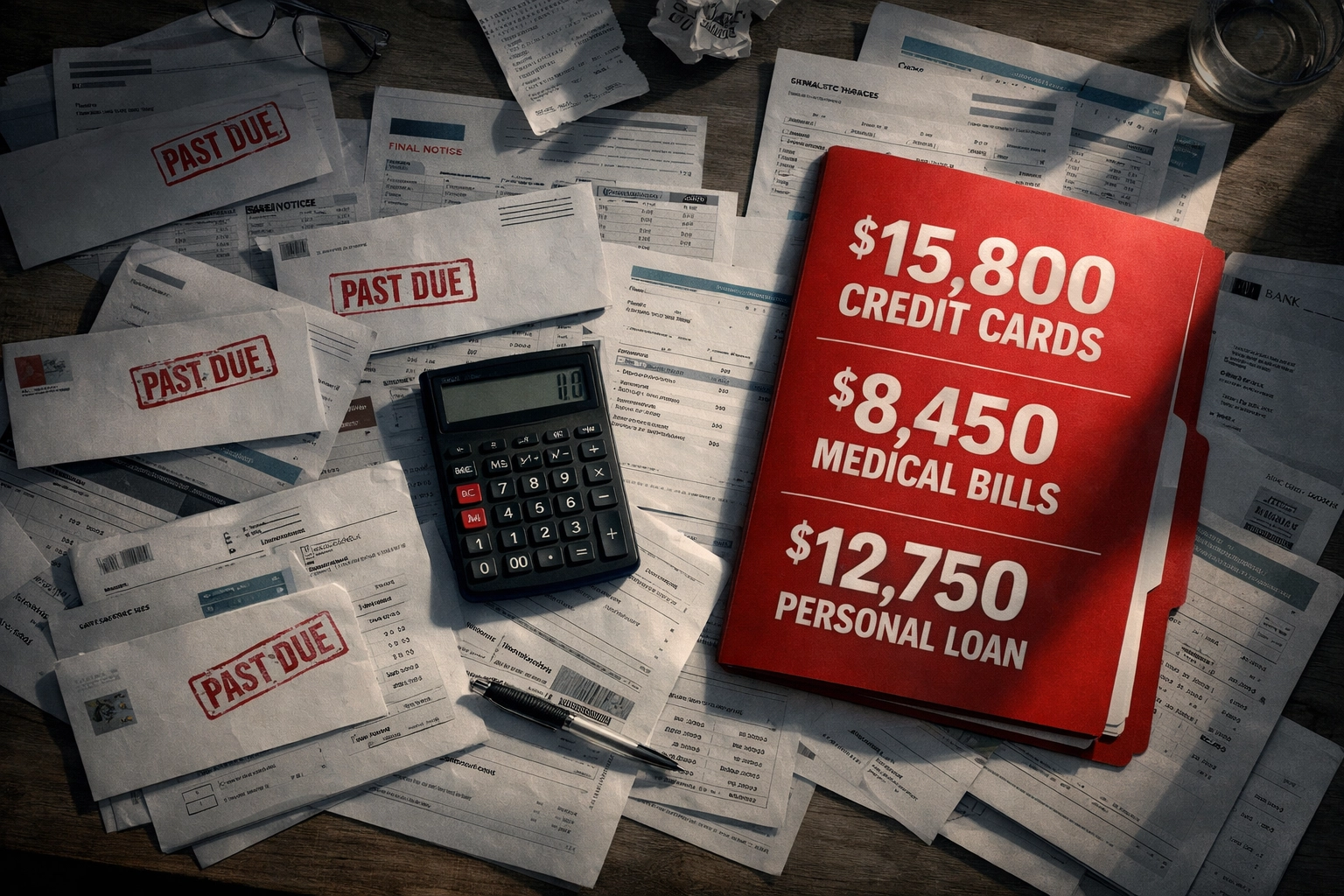

Let's get concrete. Meet Alex: HVAC technician, $50,000 in credit card and personal loan debt, $4,000/month take-home.

Traditional Debt Avalanche Approach:

Pays $1,200/month toward debt

Becomes debt-free in 4.5 years

Starts "building wealth" at year 5

By year 10, has approximately $87,000 saved (assuming 7% market returns and $1,200/month contributions post-debt)

Debt Freedom Flywheel Approach:

Funds EIUL with $600/month for 6 months ($3,600 accumulated)

Takes policy loan of $3,000 at Month 7, pays off highest-interest card

Continues funding EIUL with $600/month + former credit card payment of $180

Repeats policy loan strategy every 8-10 months, attacking next debt

By year 4.5, debt is eliminated AND has $42,000 in EIUL cash value still growing

By year 10, has $187,000 in accessible, tax-free wealth plus death benefit protection

The difference? $100,000.

That's not theory. That's the Knowing + Unrelenting Pressure = Exponential Wealth.

The Sword and Shield: Protection Meets Domination

Here's where most financial strategies collapse: They make you choose between safety and growth.

Traditional advice says "pay off debt safely and slowly" OR "take market risk to grow wealth faster." Both paths leave you exposed.

The EIUL structure gives you both weapons simultaneously:

You don't sacrifice one for the other. You deploy Strategic Growth with Guaranteed Safety.

That's not a sales pitch. That's Financial Peace of Mind engineered into the structure.

The Covenant Reality: Your Money Has a Mission

Let's bring this home with the framework that separates Warrior-Stewards from financial drifters.

From Hammurabi to Moses to Christ, the evolution of financial order teaches one lesson: Money is a tool of the Covenant, not the root of evil. The LOVE of money destroys. The strategic deployment of money for family legacy and Kingdom impact? That's the test of trustworthiness.

Consumer debt isn't neutral. It's spiritual bondage dressed in monthly statements. When you're sending $1,200/month to Chase and Capital One, you're not stewarding: you're surrendering.

The Debt Freedom Flywheel breaks that cycle by aligning your financial structure with the Law of Stewardship: Faithful in little, trusted with much.

Every policy loan you take and repay? You're recapturing interest into YOUR family banking system. Every debt you eliminate? You're freeing up resources for generational wealth transfer. Every dollar that compounds tax-free? You're building the Asset Armor your children will inherit.

Your Next Move: The Tactical Extraction

You're at a decision point. You can continue the traditional path: paying off debt slowly while the banking system profits from your discipline. Or you can become your own bank and extract yourself from their game entirely.

This isn't for everyone. It's for welders tired of funding their lender's vacation homes. It's for barbers ready to build something their kids can inherit. It's for HVAC techs who understand that strategic pressure breaks every defense.

Here's your tactical next step:

Book a strategy call. We'll map out your Debt Freedom Flywheel: specific numbers, specific timeline, specific wealth capacity targets. No fluff. No sales pitch. Just the math and the mission.

Because here's the reality: Your $50K in debt isn't the problem. The problem is the system that taught you to accept it as normal. The Debt Freedom Flywheel doesn't just eliminate debt: it weaponizes your cash flow and turns you into the bank.

The Knowing says you're already free. The Unrelenting Pressure makes it inevitable. The Exponential Wealth? That's just what happens when you finally operate with both.

Ready to break the cycle? Book your strategy call here.

🛡️⚓🥊

Comments