.jpg)

How to Be Your Own Bank: The 5-Step Family Banking Strategy That Pays Off Debt While Building Wealth Simultaneously

- Reuben Lowing

- Feb 17

- 6 min read

Here's the brutal truth nobody tells you about getting out of debt: most people who finally pay off their car loan, credit cards, and personal loans end up with a zero balance: and zero savings.

You grind for years. You skip vacations. You eat ramen. And when the dust clears? You're debt-free... and broke. Back at square one. No emergency fund. No college savings. No retirement cushion. Just relief: and exhaustion.

That's not freedom. That's survival mode with a nicer credit score.

What if I told you there's a way to pay off debt and build wealth at the same time: without working three jobs or living like a monk? A strategy that lets you become your own bank, keep your interest payments in your family instead of handing them to Mega Bank, and create a financial fortress that protects your kids and grandkids?

It's called Family Banking. And if you've got discipline (the kind that gets you to work at 6 a.m. every Monday), you can build it.

Let me show you how.

Why Traditional Debt Payoff Leaves You Broke

Most financial advice sounds like this: "Cut up your credit cards! Pay off the smallest balance first! Snowball everything!"

It works: if your only goal is to hit zero. But here's what they don't tell you:

You lose years of compound growth. Every dollar you throw at debt is a dollar that's not earning interest, building equity, or growing in value.

You're still dependent on banks. The second you need a car, or the furnace dies, or your kid needs braces: you're back at the bank, hat in hand, applying for another loan.

You never build a financial cushion. Debt payoff is a one-way street. Once the money's gone, it's gone.

It's like bailing water out of a leaking boat without ever fixing the hull. You're exhausted, but you're still sinking.

Family Banking flips the script. Instead of eliminating debt at the expense of wealth, you redirect cash flow so your money works twice: once to pay off debt, and again to build your financial future.

The Navy SEAL Way: Strategic Thinking Over Brute Force

I learned something in the Teams that applies to money just as much as it does to combat: brute force gets you killed. Strategy keeps you alive.

Most people attack debt like it's an enemy position: head-on, guns blazing, no plan B. They throw every spare dollar at the problem and hope it works out.

But the best operators don't just fight harder. They think smarter. They recon the battlefield. They protect their six. They build systems that work even when they're asleep.

That's what Family Banking is: a tactical system for families who want to win financially: not just survive paycheck to paycheck.

The 5-Step Family Banking Strategy

Here's the blueprint. This isn't theory. This is the same system I walk families through when they sit down in my office, exhausted from spinning their wheels.

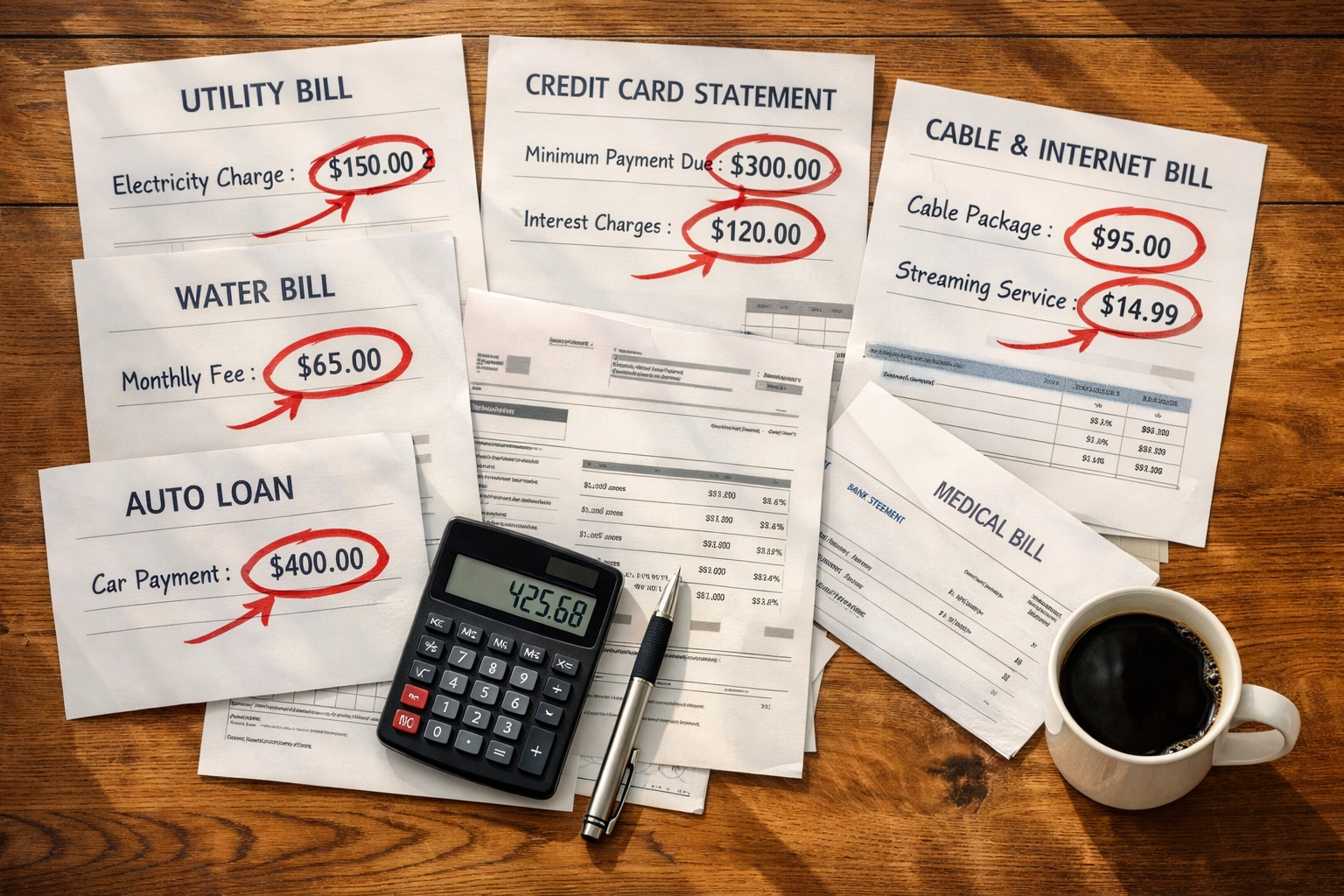

Step 1: Financial Reconnaissance – Find the Leaks

You can't fix what you can't see.

Before we build anything, we need to know where your money is actually going: not where you think it's going. Most families are hemorrhaging $300–$500 a month on subscriptions they forgot about, overdraft fees, late payment penalties, and interest charges that compound silently in the background.

What we do:

Pull your credit report and analyze every line (we use ScoreNavigator to map the full picture).

Audit your budget for "hidden leaks": the stuff that doesn't feel expensive but adds up to thousands a year.

Identify high-interest debt that's bleeding you dry (credit cards at 22%, car loans at 8%, personal loans at 12%).

This is recon. No judgment. Just data. You can't win a fight you don't understand.

Step 2: Build the Fortress – Set Up Your Family Bank

Once we know where the leaks are, we build the structure that becomes your private family bank.

This isn't a metaphor. It's a real financial vehicle: typically a high cash value life insurance policy or a specialized trust: that acts as a revolving line of credit for your family.

Here's what makes it powerful:

Uninterrupted compound growth. The money inside this "bank" earns interest and dividends even while you borrow from it. You're not stopping the compounding clock every time you need cash.

You control the terms. No credit checks. No applications. No waiting for approval. You decide when and how to borrow: and you pay yourself back, not Mega Bank.

Tax advantages. Properly structured, this vehicle grows tax-deferred and can be accessed tax-free in retirement. (Check with your CPA, but this is a game-changer for blue-collar families building wealth.)

Think of it like this: instead of renting money from a bank at their rates, you're financing your own life and keeping the interest in the family.

Step 3: Re-Route the Cash Flow – Stop Feeding the Banks

Now comes the shift.

Instead of sending $800 a month to your car loan, $250 to your credit card, and $150 to your furniture store: you redirect that cash flow into your family bank.

Here's how it works:

You borrow from your own "bank" to pay off the high-interest debt (the stuff killing you at 18%–22%).

You repay yourself at a reasonable interest rate (say, 6%–8%): but that interest goes back into your account, not Chase or Capital One.

The principal keeps growing inside your family bank, earning dividends and compound interest even while you're using it.

You're not losing the money. You're recycling it. Every payment you make strengthens your fortress instead of lining someone else's pockets.

Step 4: The Flywheel Effect – Debt Payoff + Wealth Building

This is where the magic happens.

When you pay off debt the traditional way, every dollar disappears. But when you use the Family Banking model, every dollar you "pay yourself back" becomes an asset.

Over time, this creates what I call the Debt Freedom Flywheel:

You pay off high-interest debt fast (because you're using your own capital, not waiting to save up).

The money you would've paid to banks stays in your system, growing and compounding.

As your family bank grows, you have more capital to borrow for the next big purchase: a truck, a down payment on a rental property, your daughter's wedding: without going back to a lender.

Every cycle makes you stronger, wealthier, and more independent.

This is how wealthy families operate. They don't borrow from banks: they borrow from themselves. And now you can, too.

Step 5: Secure the Perimeter – Protect What You've Built

Here's the final piece most people skip: protecting the wealth you've created.

You can build the best family bank in the world, but if you don't secure it with proper estate planning, the government and creditors can tear it apart when you're gone.

What this looks like:

Setting up a living trust to keep your assets out of probate and protect your family from legal fees and delays.

Designating beneficiaries properly so your family bank passes directly to your kids or grandkids without being touched by the IRS or lawyers.

Building a legacy plan that includes financial education for the next generation: because the worst thing you can do is hand a 22-year-old a pile of cash with no instruction manual.

This is about stewardship. You're not just building wealth for yourself. You're building a system that protects your family for decades.

Who This Is For (And Who It's Not)

Let me be straight with you: Family Banking isn't a get-rich-quick scheme. It takes discipline, patience, and commitment: the same traits that make a good welder, a good electrician, or a good HVAC tech.

This strategy works for you if:

You're tired of being in debt but you don't want to sacrifice your future to get out.

You want to build generational wealth, not just break even.

You're willing to change how you think about money and put in the work to build something real.

This isn't for you if:

You're looking for a magic bullet.

You're not ready to commit to the long game.

You'd rather blame the system than change your strategy.

No judgment either way. But if you're still reading, I'm guessing you're the first type.

Stop Renting Your Financial Future. Own It.

You've worked too hard: too many early mornings, too many late nights, too many years of grinding: to hand over your financial future to a bank that doesn't care about your family.

Family Banking isn't just about paying off debt. It's about taking back control. It's about building a system where your money works for you, not for someone else's shareholders.

And it's about creating a legacy that outlasts you.

If you're ready to stop renting and start owning, let's talk.

Book your Legacy + Financial Strategy consult here and let's build your family bank: together.

Reuben Lowing | Vice President/Agent | My Business Is Your Business/All Into Life

Comments